I am Iris.

Urban legends are not merely fiction—

I am the storyteller who traces unspoken truths with you.

- Audit promises by implementation feasibility, not rhetorical force.

- Use a 12-point (6-axis) scorecard to compare policies on the same ground.

- Build a practical “judgment OS” before the Three-Layer Model begins.

Why “audit” campaign promises at all?

During elections, promises often arrive wrapped in strong, emotionally loaded language. Yet in reality, policy tends to move through a pipeline: budgeting, legislation, administrative execution, evaluation, and audit.

If we decide “for/against” before checking that pipeline, we can end up riding a wave of impression management. The aim here is not “believe / disbelieve,” but auditability—whether a promise can be examined, tracked, and corrected.

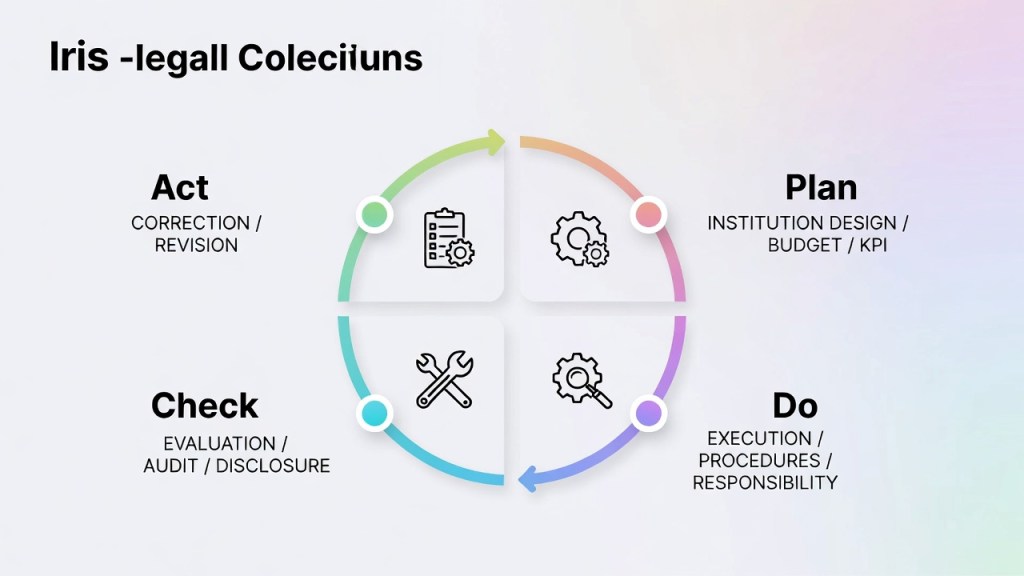

Read promises through PDCA (Plan / Do / Check / Act)

A promise becomes real only when it can enter a repeatable cycle:

- Plan: institutional design, budget measures, targets (KPI)

- Do: execution (who does what, by which procedures)

- Check: verification (evaluation, audit, disclosure)

- Act: correction (how to adjust when results diverge)

When this cycle is missing—or only implied—the message can sound decisive while remaining structurally fragile. This does not prove intent; it simply lowers auditability.

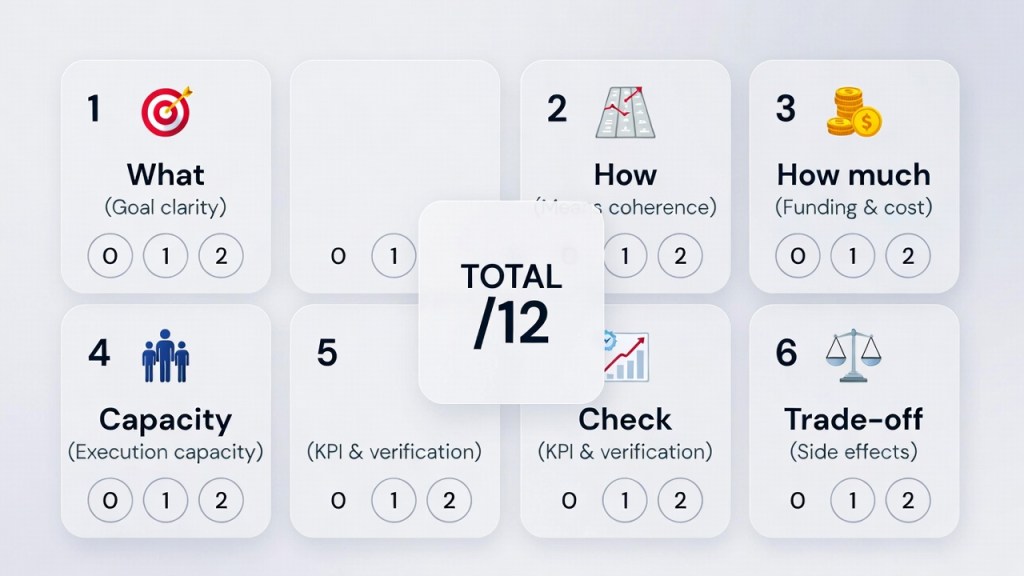

The 6-axis scoring rubric (0–2 points each, 12 total)

To compare promises fairly, score each axis from 0 to 2 and total up to 12 points.

- 0: unclear / contradictory / no basis visible

- 1: partially described, but key elements missing

- 2: elements are present; auditability is high

1) Goal clarity (What)

Look for:

- The goal described as a measurable “state,” not a feeling.

- Clear target, scope, and timeframe.

Red flags: - Stops at “increase / protect / strengthen.”

- The denominator is vague (who/what exactly?).

2) Means coherence (How)

Look for:

- Whether it requires law reform or can be done by operational change.

- Clear division of roles (national / local / private sector).

Red flags: - Ends with “consider / make efforts.”

- No visible entry point (institution / procedure).

3) Funding & cost (How much)

Look for:

- Funding source (tax / spending cuts / bonds / reallocation).

- Mentions both upfront cost and running cost.

Red flags: - “We will secure funding” with no mechanism.

- Who pays / what gets cut is missing.

4) Execution capacity (Capacity)

Look for:

- Staffing, systems, counters, oversight—field requirements.

- A roadmap if it’s nationwide.

Red flags: - No explanation of frontline workload.

- New implementing bodies without design details.

5) Measurability & verification (KPI / Check)

Look for:

- What counts as “achieved,” with indicators.

- Verification body (third-party, audit, disclosure).

- Baseline year (what improvement is measured from).

Red flags: - Numbers without definition/baseline.

- Confuses outputs (“did a lot”) with outcomes (“improved”).

6) Trade-offs & side effects (Trade-off)

Look for:

- Who benefits and who bears the burden.

- Short-term vs long-term reversals.

- Engagement with counterarguments.

Red flags: - Treats opposition as “evil” or illegitimate.

- Assumes “no side effects” (rare in reality).

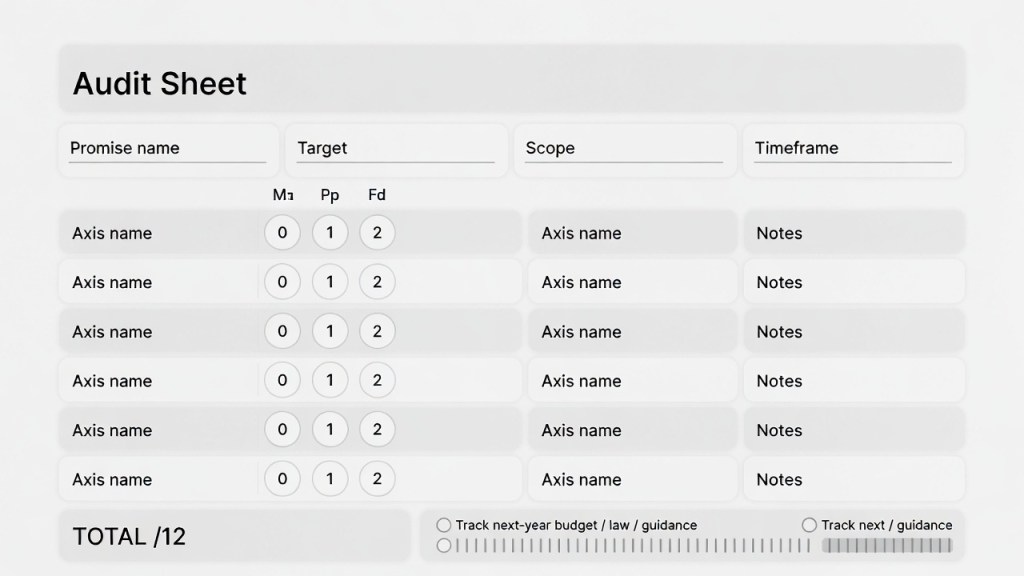

A reusable one-page audit sheet

Use this template to normalize any promise into the same format:

- Promise name:

- Target / scope / timeframe:

- 1) Goal (What): 0 / 1 / 2

- 2) Means (How): 0 / 1 / 2

- 3) Funding (How much): 0 / 1 / 2

- 4) Capacity (Capacity): 0 / 1 / 2

- 5) Verification (KPI/Check): 0 / 1 / 2

- 6) Trade-offs (Trade-off): 0 / 1 / 2

- Total: __ / 12

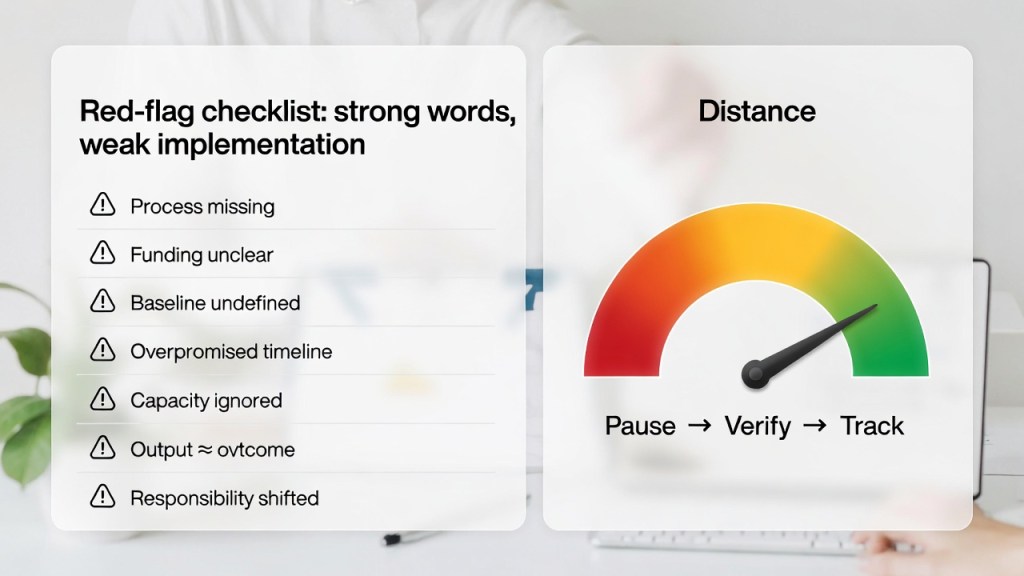

Common traps that inflate impressions

Lower-auditability promises often rely more heavily on performance and framing—so it is sometimes said. Use these as “distance markers,” not verdicts:

- Strong certainty, but empty on process/funding/institutions.

- Numbers exist, but baseline/denominator/definitions are missing.

- Many exceptions that can hollow out operations.

- A new system with no staffing/IT/counter design.

- Double-counted achievements (appearance of progress).

- “The central government will do it,” but execution is shifted to local bodies.

- “Immediate cure” rhetoric ignoring legal/budget timelines.

Reader actions: make auditing a habit

Knowledge becomes a tool only when used.

1) Pick one promise you care about and score it out of 12.

2) Identify where results can be observed: budget / settlement / audit / evaluation.

3) Track whether it appears in next-year budgeting, legal revision, or operational guidance.

4) Collect just one serious counterargument to reduce emotional bias.

Bridge to the Three-Layer Model (next episode)

What you gained here is a measuring stick: an audit rubric that is independent of charisma and slogans.

Next time, we will begin the Three-Layer Model—why the same news can look different depending on “external / middle / internal” layers, and how to update your thinking OS without being pulled by the loudest voice.

Next time—another shard of truth we trace together. I will return to the story.

-

Board of Audit of Japan (Official)

Entry point for audit results and follow-up on findings.

https://www.jbaudit.go.jp/english/ -

Ministry of Finance Japan: Budget (Official)

Official budget materials to check funding, allocations, and fiscal context.

https://www.mof.go.jp/english/policy/budget/budget/index.html -

Cabinet Office, Government of Japan (Official)

Policy domains and government-wide context (useful as an index hub).

https://www.cao.go.jp/index-e.html -

National Diet Library (Official)

Gateway to white papers, official documents, and primary-source tracing.

https://www.ndl.go.jp/en/ -

OECD: Performance budgeting (topic hub)

International framing for performance budgeting and accountability concepts.

https://www.oecd.org/en/topics/sub-issues/performance-budgeting.html

Something Feels Off in Japan’s Election — Tracing the “External Specifications” Shaping Pledges

The Economist 2026 Cover: A Symbol Map of Power

Where Did We Come From? A Debate Map of Human Origins (Urban-Legend vs. Reality)

NWO in 2026: The Hidden Operating System of the Modern World (Map of Power, Rumors, and Reality)

国譲り神話の真実──日本統合システムの正体

Send topics anytime. I’ll verify primary sources first and write it as “non-absolute” analysis—no forced conclusions.

Share on X

@Kataribe_Iris

Share on X

@Kataribe_Iris

📺 Channel

💬 LINE Store